More Top Stories

Economy

Economy

Environment

Solar power battery repairs ‘could take up to 12 months’

15 April 2024

National

Editorials

Court

Court

Crime

Police shortage leads to drop in checkpoints

9 April 2024

Editorials

Crime

National

Sarakura declared new Penrhyn MP

16 March 2024

Economy

Economy

Economy

Govt says $1.3m invested in Lady Samoa charter

22 February 2024

Local

National

Economy

Economy

Court

Environment

Mass milkfish die-off in Penrhyn raises concerns

3 April 2024

National

Regulator defends Starlink users

9 April 2024

Athletics

Local

Features

Aitutaki’s heritage preserved in new anthology

4 January 2024

League

Avatiu Eels retain Nines title

8 January 2024

Athletics

Beddoes crowned top athlete

8 January 2024

League

NRL player Dargan dies in Aitutaki motorcycle crash

24 December 2023

Economy

Editor's Pick

‘Please heed the signs’: resident makes plea to tourists

20 December 2023

League

Cook Islands set to play in new World Series

10 October 2023

Features

Editorials

Economy

Economy

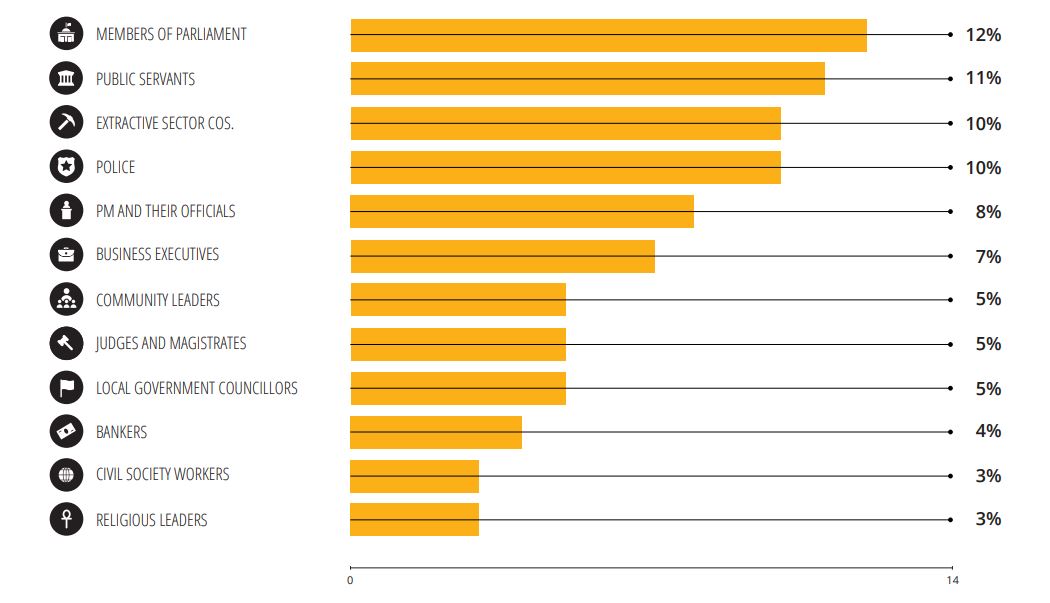

Corruption report exposes ‘bribe and sexual favours’

17 January 2023

Economy

Corruption in the Cook Islands?

21 January 2023

Rugby league

Moana target 2025 World Cup

11 November 2022

Ageing population sees pension payments rise

Friday 27 April 2018 | Written by Rashneel Kumar | Published in Economy

The government is anticipating an increase in old-age pension payments as 15 per cent of the Cook Islands workforce is heading for retirement age in the next nine years.

The government is anticipating an increase in old-age pension payments as 15 per cent of the Cook Islands workforce is heading for retirement age in the next nine years.

To continue reading this article and to support our journalism

CLICK HERE TO SUBSCRIBE NOW

for as little as $11 per month.

- Up to date and breaking news

- Includes access to Premium content

- Videos and online classifieds

Already a subscriber, click here